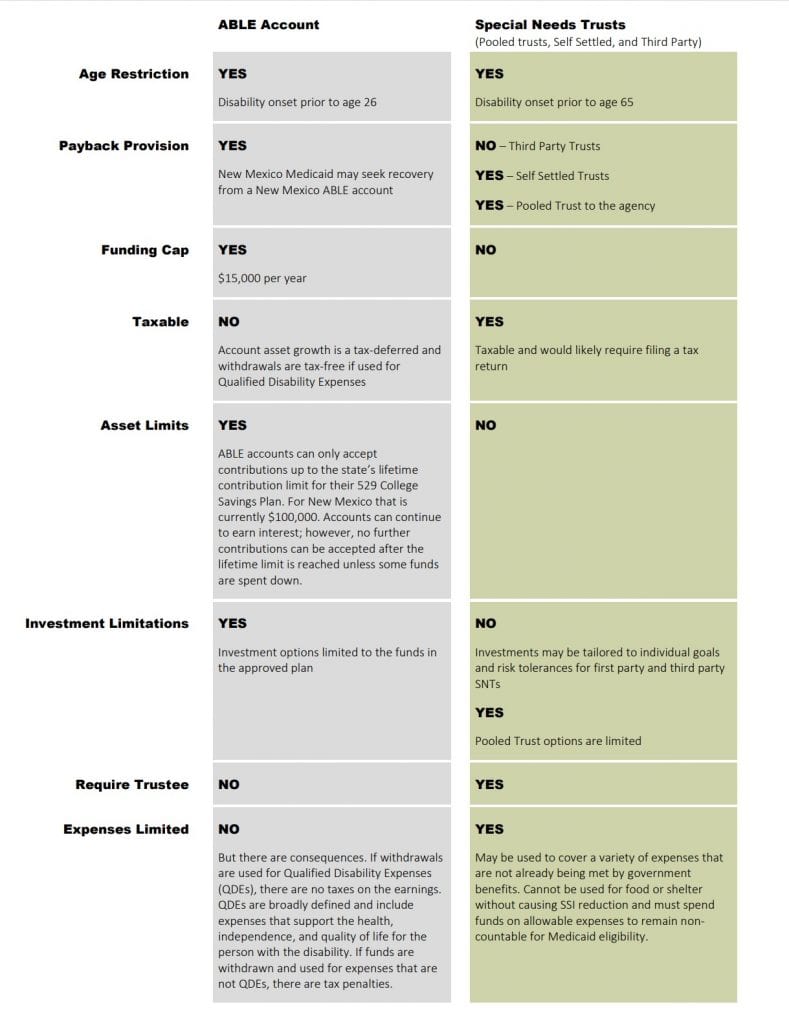

ABLE Accounts and Special Needs Trusts serve different purposes but can be used together to give the beneficiary the most freedom and independence possible. An ABLE Account is a tool that was created by federal law (the same part of the tax code where we find 529 Education plans) to help people with disabilities save some money and be as independent as possible. An ABLE account is established through a state-run program. Each individual may have only ONE ABLE account and is permitted to add no more than $15,000 per year to the account. The individual may accumulate a total of $100,000 in the account at one time and when the individual dies, any funds remaining in the ABLE account return to the state and are not distributed through the individual’s estate plan. An ABLE Account is not the place to hold large sums of money for the individual.

Comparison chart – ABLE Account vs. Special Needs Trust

Special Needs Trusts (SNTs) have no limit on the amount they can receive in a year or in the total amount that can be accumulated. A third-party SNT can also have a designated remainder beneficiary so when the primary beneficiary dies, the remaining funds can be distributed the way the Grantor wants and not to the state. An SNT is a great place to hold larger sums of money and collect larger sums from an inheritance or other source.

ABLE accounts allow the individual to use the funds for anything Medicaid and Social Security do not pay for and the individual can access the funds without permission from a trustee or other fiduciary through electronic banking. SNT’s also allow the funds to be used for anything Medicaid and Social Security do not pay for, but the beneficiary must request funds from the Trustee who will ultimately decide whether to make the requested distribution. This gives the Trustee control over the funds in the SNT and the beneficiary has no authority to direct the distributions.

With many clients, I like to use these two tools together. We establish an ABLE account and a third-party SNT for the beneficiary. That way, the beneficiary has funds in the ABLE account that they can use and contribute to as they wish, but they can’t inadvertently (or intentionally) spend large sums of money. The SNT is then the place to hold inheritance or other larger sums for the beneficiaries needs as they arise. The Trustee of the SNT can also distribute money to the ABLE account if needed. In fact, we often use these tools together to address a beneficiary’s housing. Under the Social Security Administration’s rules, SNT funds cannot be used to supplement a beneficiary’s housing costs if not on SSI (Social Security Income), but funds from an ABLE account can be used for that purpose. We can transfer funds from an SNT to an ABLE account and the beneficiary can then use the funds from the ABLE account to supplement their housing costs without penalty.

ABLE accounts and SNT’s are just few of the tools we have in our toolbox to help people with disabilities and their families ensure that individuals have the best life possible. Like many things, there is no one single solution that works for everyone. Sometimes it makes the most sense to use more than one tool to solve the problem, and we are happy to help you find the tool or tools that work best for your situation.