During the 2020 election campaign, President Joe Biden proposed certain changes to the Internal Revenue Code, which among other things, could change the current law on estate and gift taxation. There are two possibilities you should be aware of: the lowering of the estate tax exemption and the elimination of the stepped-up basis on death. The first would affect only multi-millionaires, but the second could have an impact on more modest estates and their heirs.

The first change would reduce the current estate tax exemption levels. Before the Tax Cuts and Jobs Act of 2017, the estate tax exemption level was $5 million, which increased each year based on inflation. The exemption was doubled for married taxpayers. Under the Tax Cuts and Jobs Act of 2017, the estate tax exemption amounts more than doubled – the exemption for a single taxpayer in 2021 is $11.7 million and $23.4 million for married taxpayers. As long as your estate is valued under the exemption amount, no federal estate taxes are owed, and the vast majority of estates do not owe any tax. President Biden has expressed an interest in lowering the estate tax exemption. It could be more than halved to $5 million or reduced to the previous 2009 exemption of $3.5 million for individuals and respectively $10 million or $7 million for married taxpayers.

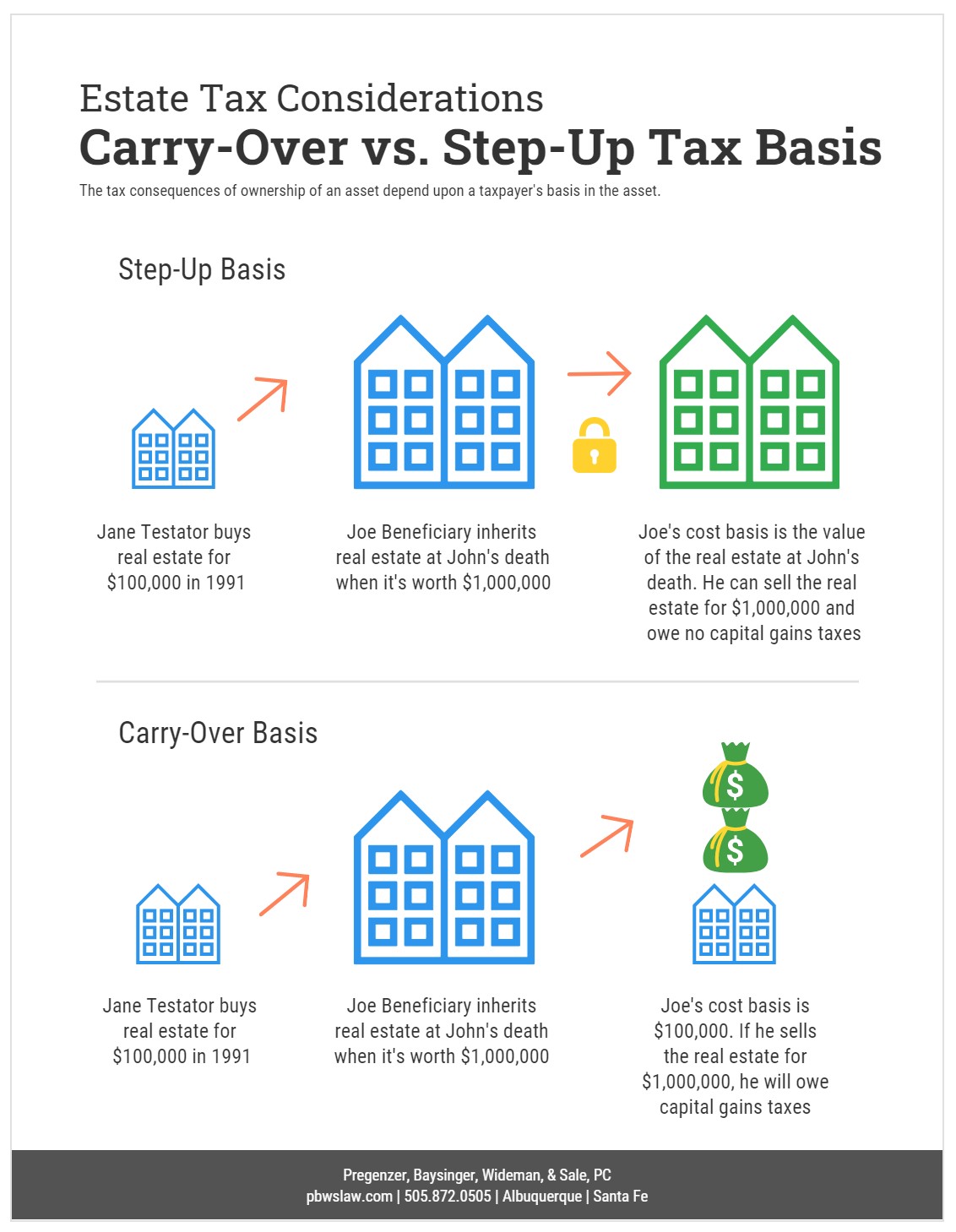

Another possible tax change is how property is valued when it is passed on at death. “Cost basis” is the monetary value of an item for tax purposes. When determining whether a capital gains tax is owed on a property, the basis is used to determine whether an asset has increased or decreased in value. For example, if you purchase a stock for $10,000, that is the cost basis. If you later sell it for $50,000, you will have to pay taxes on the $40,000 increase in value.

Under current law, when a property owner dies, the cost basis of the property is “stepped up.” This means the current fair market value of inherited assets becomes the “new” basis in the beneficiaries hands. For example, suppose you inherit a house that was purchased years ago for $100,000 and it is now worth $1 million. You will receive a step up from the original cost basis from $100,000 to $1 million. If you sell the property right away for its fair market value, you will report little to no gain on your taxes because your basis would be the $1 million current fair market value.

According to an article in the New York Times, the current administration may propose to eliminate the basis step-up rule. In the past, it was difficult to determine the original cost basis of some property, but in the digital age, this information is more easily gathered. The change could result in tax increases for some people inheriting property which has risen significantly in value. If the basis step-up rule is eliminated, your tax outcome would be drastically different. Under President Biden’s plan, in the same real estate scenario as above, your inherited property would be assessed on a carryover basis, meaning you would carryover the basis in the real estate at $100,000. If you immediately sold the real estate for its fair market value of $1 million, you would report a taxable gain of $900,000 (sale price of $1 million less the carryover basis of $100,000).

Another question is whether either of these changes will be made retroactively. It is unlikely, but possible, if Congress changes these rules later in the year, they could be made retroactive to the first of the year.

It is unclear whether such proposals are likely to succeed in Congress. Nonetheless, the estate tax exemptions under the Tax Cuts and Jobs Act of 2017 are scheduled to sunset on December 31, 2025. Consequently, it is important for taxpayers whose estates are subject to estate taxes to speak with an estate and tax planning attorney to maximize the wealth they pass on to their friends and family.